About JAEPSJournal of Applied Economics and Policy Studies (JAEPS) is an open-access, peer-reviewed monthly academic journal hosted by the Peking University Research Centre for Market Economy (RCME) and published by EWA Publishing. Centered on real-world economic practice, the journal integrates three core research dimensions: practical application of economic theories, measurable economic output of empirical research, and evidence-backed policy formulation value of rigorous academic outputs. Beyond economic and decision-making value, it highlights industrial empowerment, standardized governance, cross-border exchange and demonstration promotion value of economic research; these multi-layered research values are delivered to university economics researchers, government economic policymakers, enterprise industrial consultants and financial analysts via standardized quantitative research paradigms, industrial decision references and cross-border academic communication channels.For more details of the JAEPS scope, please refer to the Aim&Scope page. For more information about the journal, please refer to the FAQ page or contact info@ewapublishing.org. |

| Aims & scope of JAEPS are: ·Economics ·Management ·Finance & Accounting ·Interdisciplinary Fields |

Article processing charge

A one-time Article Processing Charge (APC) of 450 USD (US Dollars) applies to papers accepted after peer review. excluding taxes.

Open access policy

This is an open access journal which means that all content is freely available without charge to the user or his/her institution. (CC BY 4.0 license).

Your rights

These licenses afford authors copyright while enabling the public to reuse and adapt the content.

Peer-review process

Our blind and multi-reviewer process ensures that all articles are rigorously evaluated based on their intellectual merit and contribution to the field.

Editors View full editorial board

Beijing, China

xqin@pku.edu.cn

London, UK

canh.dang@kcl.ac.uk

Edinburgh, UK

B.Adamolekun@napier.ac.uk

Macau, China

qiangli@cityu.edu.mo

Latest articles View all articles

Beginning with archaeological discoveries related to Wu culture, this paper provides an in-depth interpretation of its connotations and cultural significance. The Ode to Wudianyuan written by Dr. Binzi offers a profound exposition of Wu culture and serves as an important reference for understanding its essence. Taking the development of the Wudianyuan cultural industry as a case study, this paper examines the prospects for Wu culture industrialization from four perspectives: strengths, weaknesses, opportunities, and threats. Furthermore, it presents a detailed discussion of the initial vision for the Wudianyuan project and analyzes its current development dynamics and future prospects.

Using panel data on prefecture-level cities with airports in China from 2011 to 2023, this study employs a two-way fixed effects model to examine the relationship between airport traffic and urban consumption carrying capacity. The results indicate that passenger throughput has no robust and statistically significant effect on the total retail sales of consumer goods. In the tourism revenue model, both airport traffic and hub-airport pressure exhibit significantly positive effects, reflecting the regional gateway effect. In the wholesale and retail sector model, the coefficient of hub-airport pressure is negative but statistically insignificant for cities served by non-hub airports. These findings suggest that whether airport traffic can be converted into local consumption depends largely on a city's capacity to absorb and accommodate demand through its tourism, commercial, and service sectors.

The intelligent business environment is driving instructional practices in higher vocational e-commerce programs from a uniform teaching schedule toward differentiated competency development. Conventional evaluation methods are no longer capable of accurately reflecting students' developmental trajectories in tasks such as e-commerce operations, digital marketing, customer service, and data analytics. To address the need for evaluating the effectiveness of tiered instruction, this study develops a fuzzy comprehensive evaluation system centered on competency growth and supported by evidence generated from intelligent learning environments. The proposed framework integrates occupational competency standards, course task data, learning platform behavioral records, and teacher evaluation information to establish a tiered evaluation index system. It further incorporates a hybrid weighting approach combining subjective and objective methods, a contextualized membership degree calculation model, and a comprehensive evaluation model for instructional effectiveness. The system effectively addresses the challenges of ambiguous evaluation boundaries, heterogeneous evidence sources, and substantial differences across instructional tiers. It provides a practical framework for improving teaching quality, supporting differentiated student development, and implementing intelligent assessment in higher vocational e-commerce education.

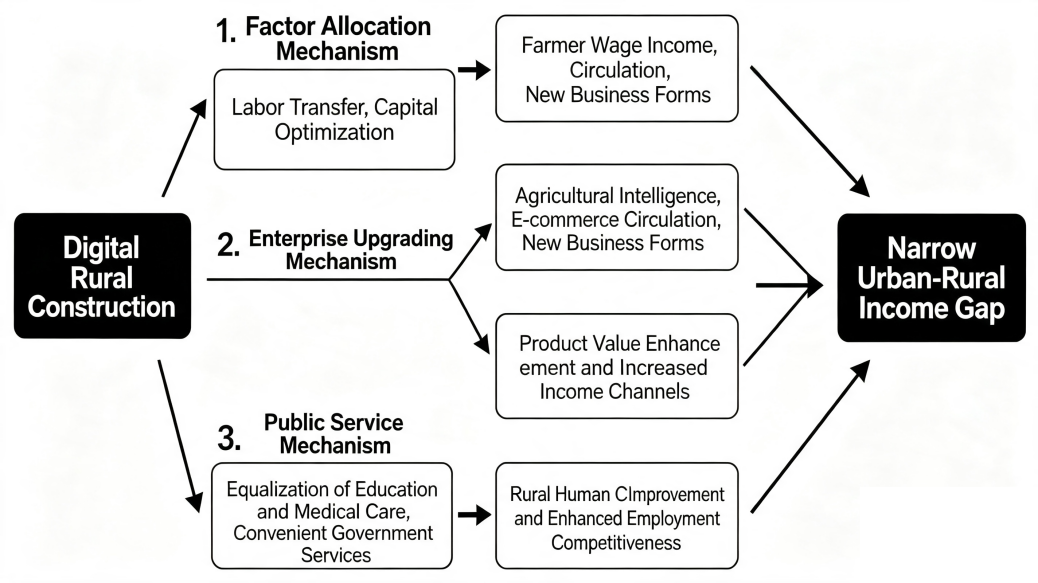

Digital rural development has become one of the key initiatives for advancing rural revitalization and addressing unbalanced development. This study employs the Theil index to measure the urban–rural income gap and investigates the mechanisms and spatial effects of digital rural development using the entropy weighting method, spatial econometric models, and the instrumental variable approach. The results indicate that digital rural development contributes to narrowing the urban–rural income gap and exhibits significant spatial spillover effects. In addition, higher urbanization rates and greater human capital help reduce the income gap between urban and rural areas, whereas long-term fiscal support for agriculture does not produce a statistically significant effect. This study provides empirical evidence to support the acceleration of digital rural development and the promotion of integrated urban–rural development.

Volumes View all volumes

2026

Volume 19April 2026

Find articlesVolume 19March 2026

Find articlesVolume 19June 2026

Find articles2025

Volume 18May 2025

Find articlesVolume 18September 2025

Find articlesVolume 18August 2025

Find articlesAnnouncements View all announcements

Journal of Applied Economics and Policy Studies

We pledge to our journal community:

We're committed: we put diversity and inclusion at the heart of our activities...

Journal of Applied Economics and Policy Studies

The statements, opinions and data contained in the journal Journal of Applied Economics and Policy Studies (JAEPS) are solely those of the individual authors and contributors...

Indexing

The published articles will be submitted to following databases below: